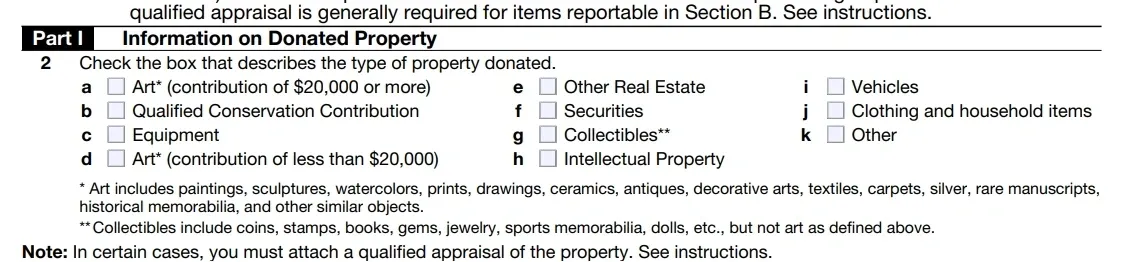

When property owners choose deconstruction over demolition, they unlock powerful tax benefits through charitable contributions that can offset, or sometimes even exceed, additional project costs. Yet the pathway from salvaged materials to legitimate tax deductions is fraught with technical requirements that, if overlooked, trigger complete disallowance of these benefits. The IRS has transformed noncash charitable contributions into an enforcement priority, wielding strict procedural standards as their primary weapon against perceived abuse.